At some point we might be able to talk about the economy without focusing on the tariff situation but that time has not yet arrived. It has become nearly impossible to determine the policy in place for more than a day. The investment community has come to call these the TACO tariffs (Trump Always Chickens Out). As one would, expect this term infuriates Trump and he may stick with them in the future to make a point. The assertion is that he changes his mind when presented with the impact of the decisions. It may also just be part of the negotiating process.

It is probably time to revisit the motivations behind the tariff struggle as the priority ranking seems to shift on a daily basis. From the beginning there have been three rationales or justifications for the tariff policy. The first is an attempt to recover some of the manufacturing base the US has lost over the last several decades. The manufacturing sector once accounted for almost 25% of the nation’s GDP (in the 1960s and 1970s) but that share has shrunk to 10%. Imports played a major role in this decline but it was not the only reason for all the job loss (some 20 million in the 1990s alone). Technology replaced a great many of those industrial jobs but so did outsourcing and imports. The thinking now is that restricting imports would allow the recovery of the industrial sector. It is clear that restricting imports or making them more expensive will help but there are many other changes that would need to take place – changes the manufacturer has been asking for over a several decade period. Labor force expansion, infrastructure support, assistance in developing R&D, regulatory relief, tax relief and so on.

The second motivation that has been offered for the tariffs focuses on national security. The US has become dangerously dependent on other nations for key supplies and resources. The vast majority of the chips that are used in our weapons systems come from imports. Most of the time these are supplied by nations allied with the US but not always. Of course, these chips also support the entire US tech sector and there have been efforts to stimulate production of these devices in the US. It is not just chips, the US is way behind in developing solar panels, electric vehicles, rare earth commodities and so on. It is assumed that placing tariffs on products from other nations will encourage the expansion of US production but that process is complex and slow at best.

The third stated motivation for a tariff policy is that it provides room to negotiate. Trump has a reputation as a dealmaker and the assumption is that he can use the tariff threat to get want he wants from other nations. Take the issue of drugs coming from Mexico. He threatened high tariffs on Mexico if it did not step up its efforts to halt the flow and the 20% tariff on China is based on demands that China address the export of chemicals used in the production of fentanyl. The challenge with this motivation is that it is all based on who has the leverage. Sometimes that is the US and sometimes it isn’t. The US is nearly always the demand side of this equation and China is generally on the supply side. The US needs and wants what China (and others produce) but these nations need access to the US consumer. The question is who needs who the most.

What does all this mean for construction – residential and non-residential? The two salient factors include the impact this has on construction materials and the impact this may have on demand. Obviously, higher prices for steel, aluminum, lumber, appliances and equipment add to the cost of a home or project. The average price of a home is still north of $400,000 but there is considerable regional variation (in California it is $830,000 and in Mississippi it is $267,000). Commercial prices are all over the place as well. Not only have materials gained but so has labor with construction workers averaging $25 an hour (nationally). Home buyers have been daunted by high prices as well as expensive mortgages and that is likely to intensify as long as yields on the ten-year bond keep rising.

To the US business community, the most vexing part of the tariff situation is the constant fluctuation. A tariff threat is issued that would radically change the supply chain and then a week or two or three later it is rescinded. China was to be hit with a 143% tariff and it was subsequently altered and lowered to 30%. The European Union faced a 50% tariff deadline on a Friday but by Monday there was a month-long delay. No business decision can be made under these conditions so the majority of companies just go into a period of stalling and delaying. This is especially true of those in construction as they need to predict costs months and even years in advance. In addition to this concern there is the fact that these tariffs are ephemeral. They have all been created by a stroke of the Presidential pen and they can all be undone the same way. Trump constantly changes his mind but the bigger worry is what happens when he leaves office. When Biden took over from Trump, he negated 40% of the executive orders signed by Trump and when Trump came back to power, we undid 40% of Biden’s. No company will invest in producing something if they think they will lose that competitive edge in a few years.

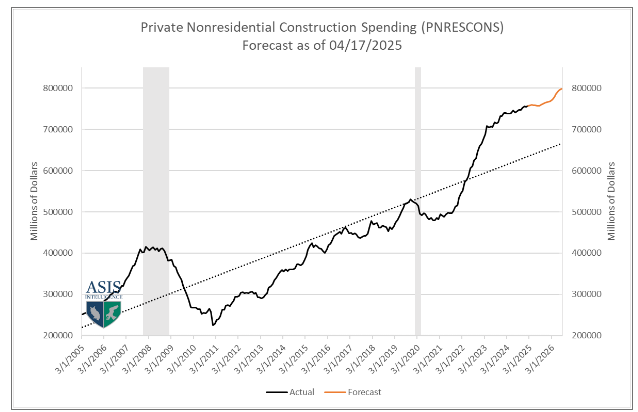

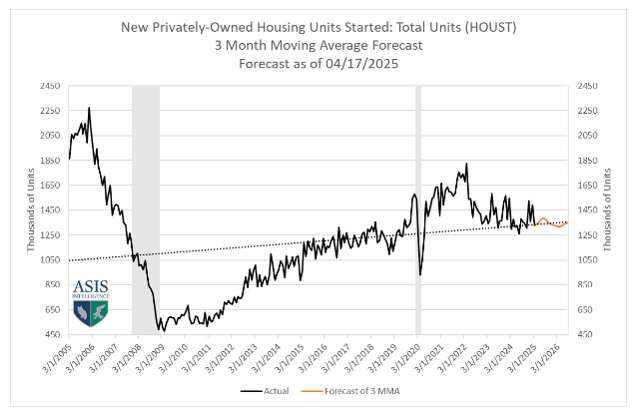

As these charts suggest there is still considerable growth in the non-residential category but marginal growth in residential. The good news is that Armada’s data shows growth in both sectors and our accuracy rate on these projections have been at 97% to 98% month after month.